A sunk cost is money, time, or effort already spent that cannot be recovered. The sunk cost fallacy is the pattern of continuing a course of action because of what has already been invested, rather than what lies ahead. It persists not because people are irrational but because most decision processes have no mechanism to separate past expenditure from future uncertainty.

The standard explanation is correct but useless. Every MBA graduate knows the sunk cost fallacy by name. Every organisation still falls for it. Knowing the name of the trap has not reduced its frequency, because the trap is not in the thinking. It is in the process.

I have spent fifty years advising organisations on consequential decisions. The sunk cost pattern repeats across every sector I have worked in. And in every case, the people were not the problem. The apparatus they were operating within was the problem. The Universal Decision-Making Method that Roger Estall and I developed provides the structural fix: a process that forces past expenditure out of the frame and replaces it with a forward-looking test of sufficient certainty.

What the sunk cost fallacy is

The mechanism underneath is loss aversion. Kahneman and Tversky established in 1979 that people feel losses roughly twice as strongly as equivalent gains. Abandoning a project you have invested in registers as a loss, even when continuation is the more expensive path. This is well documented at the individual level. At the organisational level, the effect compounds, because the investment is embedded in budgets, contracts, job titles, and board commitments.

That compound effect is where sunk cost bias turns from a psychological tendency into a governance problem: old spend acquires a moral voice, and the room defends a programme nobody believes in.

The Anglo-French Concorde programme is the canonical example, cited so frequently that economists named the pattern after it: the Concorde fallacy. By the early 1970s, projections showed the aircraft would never be commercially viable. Both governments continued funding. The investment already committed, over £1 billion in 1960s money, had acquired its own political constituency. Cancellation would have been an admission that the money was wasted. Continuation was framed as protecting the investment. The investment was already gone.

At the individual level, sunk cost reasoning is a psychological tendency you can, in theory, override with discipline. At the organisational level, it becomes structural. Walking away from a programme does not just write off money. It threatens the people whose roles depend on the programme continuing, the suppliers whose contracts depend on it, and the executives who approved it.

Kodak built a global business on chemical film processing. When digital photography emerged, a technology Kodak's own engineers had pioneered in 1975, the company kept investing in film infrastructure. Chemical plants, retail partnerships, processing revenue: all of it was treated as evidence that film would endure. The assumption that film revenue was structurally durable was never surfaced, never tested. Kodak filed for bankruptcy in 2012. The apparatus had been analysing the wrong question.

Boeing's 737 programme is the industrial-scale version. Decades of investment in the airframe, the manufacturing tooling, the FAA type certification, and the airline fleet compatibility created an assumption so deeply embedded it was invisible: that the platform could accommodate modifications it fundamentally could not. The 737 MAX was not a design failure in isolation. It was a sunk cost failure dressed as engineering pragmatism.

Why knowing about sunk costs does not prevent them

Every popular guide to the sunk cost fallacy ends with the same advice: recognise the bias, evaluate the decision on its future merits alone, walk away if the numbers do not work. This is like telling someone with a broken leg to walk it off. The diagnosis is correct. The prescription ignores the mechanism.

Consider a CFO at a logistics company, facing a fleet replacement decision. The company has spent $150,000 on a fleet optimisation study. The study recommended keeping the existing diesel fleet for three more years. When fuel costs and emissions regulations shifted six months later, any proposal to accelerate replacement was met with the same question: "But the study said three years." The $150,000 had become part of the decision's furniture. The sunk cost was not the fleet. It was the analysis already invested in defending the fleet.

Awareness-based interventions fail because the decision process itself has no mechanism to strip past investment from the frame. The risk register carries the investment history. The business case references prior expenditure as justification for continuation. The steering committee has "protect shareholder value" as a standing agenda item, and protecting shareholder value somehow always means protecting whatever was started last quarter. The result is the same deadlock that produces analysis paralysis: a process that can generate analysis but cannot generate a decision.

The decision process that lets sunk costs persist

The real problem is architectural. Risk registers, feasibility studies, options analyses: the standard apparatus of organisational decision-making asks "How do we manage the risks of what we are doing?" It does not ask "Should we still be doing this at all, given what we now know?"

That second question requires separating past expenditure from future uncertainty. Most decision-making frameworks are incapable of this separation because they were not designed for it. They were designed to document due diligence, to demonstrate that the organisation considered the risks, to satisfy regulators and auditors that the process was followed. None of that requires testing whether the original rationale still holds.

The apparatus asks "How do we protect what we have spent?" It should ask "Does this serve our Purpose regardless of what we have spent?" The people operating within this apparatus are not irrational. They are responding rationally to a process that rewards continuation and penalises abandonment. The sunk cost fallacy, in organisations, is less a thinking error than an incentive structure masquerading as rigour.

How to strip past investment from a decision

The question that breaks a sunk cost deadlock is deceptively simple: "What is this organisation actually for?"

Purpose, as I use the term, is not a mission statement or a strategy document. It is the reason the organisation exists: the outcome it is meant to produce. When that question is asked honestly, past investment becomes irrelevant. A hospital exists to improve patient outcomes. Whether the hospital spent $4 million on a records system that does not work has no bearing on whether that system serves the purpose. A newspaper exists to inform its readers. Whether the newspaper invested decades in a print distribution network has no bearing on whether print still serves that purpose.

The NHS National Programme for IT, launched in 2002 with a budget of £12 billion, was meant to deliver integrated electronic health records across England. By 2006, hospitals were rejecting the centralised systems and clinicians found them unusable. The investment in contracts, infrastructure, and political credibility had acquired its own weight. The Purpose was improving patient care. The process had become protecting the programme. When NPfIT was finally dismantled in 2011, roughly £10 billion had been spent on a system that did not serve the purpose it was built for.

When Purpose is the frame, the question is not "How do we recover what we spent?" The question is "Does continuing serve what we exist to do?" Sunk costs disappear under that test, because they answer a question nobody asked.

I have walked that test through HS2's numbers, GBP46.8 billion already gone and both remaining futures priced honestly, in sunk cost and decision making.

From hidden assumptions to sufficient certainty

"We should continue because we have invested $2 million" is not a fact. It is an assumption: that past investment predicts future return. Most of the time, nobody states this assumption out loud. It operates as background premise, shaping every option the organisation considers without ever being examined.

The single most useful question I have encountered in fifty years of advising organisations is this: "What are the assumptions we are making here?" In my experience, the question is almost never asked. Yet when it is, the sunk cost reasoning surfaces immediately. "We assume the platform will eventually pay off." "We assume the market will return to where it was." "We assume we cannot get this capability any other way." Each of these is testable.

Not all assumptions carry equal weight. Some, if wrong, destroy the decision. Others barely matter. A test of significance, asking how much the outcome depends on this assumption holding true and how confident we are that it will, sorts the critical from the trivial. For sunk cost assumptions, the test is pointed: does the past investment actually predict the future outcome? If the answer is "we do not know," three options remain. Obtain more information. Modify the decision to reduce dependence on that assumption. Or make a different decision entirely. Each produces forward motion. None requires throwing good money after bad.

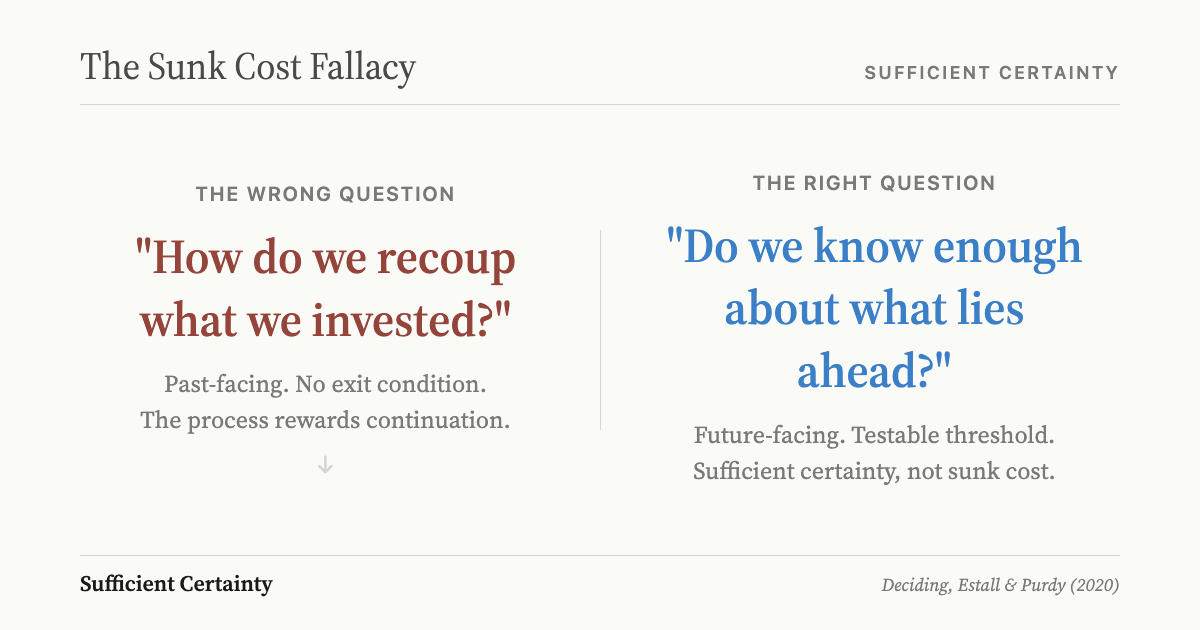

Sunk cost thinking asks the wrong question. "How do we recoup what we invested?" is a question about the past. "Do we know enough about what lies ahead?" is a question about the future. They are not the same question, and they do not have the same answer.

Sufficient certainty, the threshold at which you know enough to act, has nothing to do with the size of the prior investment. A project with $50 million sunk and a project with $50,000 sunk face the same test: have you identified the assumptions your decision depends on, assessed their significance, and either accepted them or reduced them? If yes, decide. If no, you have specific work to do, and that work is not "analyse more." It is "test these assumptions."

California's high-speed rail project is a study in untested assumptions. Voters approved a $33 billion bond in 2008 for a train connecting Los Angeles to San Francisco in under three hours. The assumptions were specific: construction costs, ridership projections, federal co-funding, private-sector investment. By 2022, the projected cost had exceeded $100 billion, the timeline had slipped by decades, and none of the original assumptions held. Yet each cost overrun was met with a revised plan, not a re-examination of the assumptions the project rested on. The investment in planning, land acquisition, and early construction segments had become the argument for continuation. Nobody asked "Do we know enough about what lies ahead?" They asked "How do we protect what we have already built?"

The opposite case exists. In 2024, NASA refused to let programme investment determine whether two astronauts would fly home aboard a spacecraft that had shown thruster anomalies. The agency chose to bring its astronauts home on a different vehicle rather than trust a system that had not demonstrated sufficient certainty. Billions were invested in the Starliner programme. The sunk cost did not enter the decision. That is the test working.

One discipline completes this test: design monitoring before you implement. If a decision rests on assumptions about the future, monitoring must detect when those assumptions stop holding, before the organisation creates a new sunk cost on top of the old one.

Grant Purdy is the co-author, with Roger Estall, of Deciding (2020), and the architect of the Universal Decision-Making Method.

If you have a decision you are working through, the Walk can help.

Start a Walk